Jews own America https://t.co/DVOFisqYNv

— Lou Ferreira (@LouFerreira9) March 24, 2024

Money

G. Edward Griffin: Why Banks Want the System to Crash, Dollar to Plummet and For You to Be Desperate

21 Feb 2024

Are banks deliberately engineering financial crises? Is the Federal Reserve part of a scheme to erode your wealth? Dive into these questions with G. Edward Griffin, the author of “The Creature from Jekyll Island,” in a must-watch interview with Daniela Cambone. Griffin reveals the shocking truth about how crises benefit the elite, the hidden agenda behind the erosion of the dollar, and the unsettling reset reshaping our world.

He even challenges the medical industry’s approach to cancer treatment, suggesting a profit-driven model over genuine cures. This video is for anyone who suspects that not all is as it seems in our financial and health institutions.

Watchdog: Push Back to Tyranny & Control Increases in 2024 with Catherine Austin Fitts, 30 December 2023 (62 mins)

BY RHODA WILSON

Jan 7, 2024

While preparing The Solari Report’s annual wrap-up, there were so many stories of people pushing back in 2023 against Mr. Global’s plans that a separate summary page had to be made to list them all.

People who would never believe us that Mr. Global’s agenda was as bad as it is, realised in 2021 that: “It really is [that] bad.” In 2022, they thought about what they could do about it and in 2023, they realised it was “kill or be killed” and started to do something about it.

Catherine Austin Fitts is an American investment banker and former public official who served as managing director of Dillon, Read & Co. and United States Assistant Secretary of Housing and Urban Development for Housing during the Presidency of George H.W. Bush. She is the president of Solari, Inc., publisher of The Solari Report, and managing member of Solari Investment Screens. She also co-founded Sea Lane Advisory.

Solari’s website published articles, reports and videos. As well as on Solari’s website, videos are uploaded on Solari’s YouTube channel HERE and Rumble HERE.

On 30 December, Austin Fitts joined Greg Hunter, host of USA Watchdog, to discuss The Solari Report’s publication titled ‘The Future of Financial Freedom’ which is a wrap-up for the first quarter of 2023. The publication is available to Solari Report subscribers.

During this conversation, she also spoke about property confiscation and total control – the enslavement of the world – by the United Nations through the World Health Organisation and other affiliated organisations.

It is well worth watching Austin Fitts’ interview below as it covers broader geopolitical events from a financial or monetary perspective. The subject of weather warfare even entered the discussion. As you can imagine, what we have noted in this article doesn’t do the information she shares justice.

In the interview above, Austin Fitts briefly spoke about David Rogers Webb’s ‘The Great Taking’. Austin Fitts had recently interviewed Webb. She doesn’t agree with Webb’s analysis of money velocity and commented in her description of the interview: “I will review a list of ‘takings’ covering all asset classes with Dr. Farrell in the ‘Annual Wrap Up – News, Trends & Stories Part I in January’.”

She also told Hunter that while preparing for The Solari Report’s assessment of 2023, its annual wrap-up, “our number one story, the top story for 2023 … was ‘2023: The Year of Push Back’,” she said.

The number of reports of pushback in 2023 “was so long, it was so big, that we had to make a special page and move the other 19 stories to a whole other section, another page,” Austin Fitts said. There are so many areas of pushback, she added.

“What happened in 2023 … [is] people who would never believe you and me that it was this bad but in 2021 they realised: ‘Oh, it really is this bad’. And during 2022 they started to go to work on ‘What are we going to do about it’. And 2023 is when they decided ‘Okay, this is kill or be killed; we have to push back because there’s no going along with this because they’re trying to kill us, number one, and they’re trying to take all of our stuff, and we can’t let them’,” she said.

In The Solari Report’s first ‘Money & Markets’ report for 2024, Austin Fitts and John Titus discussed some of the “push back” stories. You can watch a short preview HERE.

Below are The Solari Report’s quarterly wrap-ups for 2023 which are still to be updated for quarter four. They comprise a list of hyperlinked reports, interviews and articles. At the time of writing, the 2023 annual wrap-ups had not yet been published, or, at least, were not visible to non-subscribers.

- The Best of the Solari Report 2023 – The Weekly Interviews, 7 December 2023

- The Best of the Solari Report 2023 – The Special Reports, 14 December 2023

- The Best of the Solari Report 2023 – The Hosts, 19 December 2023

- The Best of the Solari Report 2023 – The Wrap Up Themes, 21 December 2023

- The Best of the Solari Report 2023 – News Trends & Stories with Dr. Joseph P. Farrell, 28 December 2023

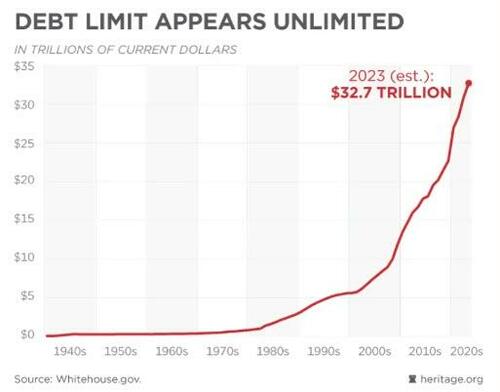

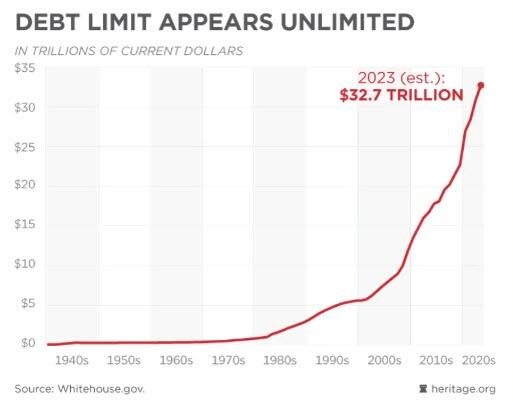

US national debt has reached a record high – hitting $34 trillion for the first time in history.

https://www.shtfplan.com/headline-news/americas-empire-of-money-has-reached-the-endgame

Jan 5, 2024

This article was originally published by Michael Snyder at The Economic Collapse Blog.

We did it, Joe! It took a tremendous push down the stretch, but the U.S. national debt was able to hit the 34 trillion dollar mark before the end of 2023. At this moment, I am just so overwhelmed that I don’t know who to thank first.

Over the past few years, Joe Biden, Kamala Harris, Chucky Schumer, Nancy Pelosi, Kevin McCarthy, and so many other hard-working spenders have been instrumental in helping us reach this remarkable achievement. And we never would have gotten here without the relentless help of CNN, MSNBC, Fox News, the New York Times, the Washington Post, and all of the other mainstream news outlets that kept assuring the American people that it was okay to steal trillions of dollars from our children and our grandchildren.

Of course, I am being quite facetious. The truth is that what we are doing to future generations of Americans is beyond criminal. We are literally committing national suicide, but each election cycle most of the same big-spending politicians just keep winning over and over again.

Those on the other side would argue that it has been absolutely necessary to borrow and spend so much money.

If we had not propped up the U.S. economy with giant mountains of borrowed money, it would have collapsed long ago.

In addition, spending so much money allows us to project military and economic power all over the planet. If we only spent what we brought in, America’s standing in the world would be greatly reduced.

Having the primary reserve currency of the world is an enormous source of power, but now that power is fading.

Nations all over the globe are starting to move away from using the U.S. dollar in international trade, and they are becoming a lot more hesitant to buy our debt.

You can only borrow and spend so much before the entire Ponzi scheme collapses, and at this moment we are more than 34 trillion dollars in debt…

US national debt has reached a record high – hitting $34 trillion for the first time in history.

Data published by the Treasury Department Tuesday showed that outstanding federal borrowing soared to $34.001 trillion on December 29, just weeks ahead of Congress deadlines for new federal funding plans.

The staggering figure, which is a major point of contention between Republicans and Democrats, is equal to $101,233 in federal debt for every person in America, according to the Peter G. Peterson Foundation.

So if there are four people living in your household, your share of the national debt is more than $400,000.

And every day the debt gets even larger. As Wolf Richter has pointed out, the size of the national debt has increased by 2.5 trillion dollars in just the last seven months…

The total US national debt spiked by $1.0 trillion in 15 weeks since September 15, to $34.0 trillion, according to the Treasury Department’s figures this afternoon. In the seven months since the debt ceiling was lifted, the national debt spiked by $2.5 trillion.

These are huge gigantic numbers that are piling up as a result of the incredible hard-to-fathom daredevil reckless shake-your-head deficit spending by Congress.

Overall, the U.S. national debt has grown by $6.25 trillion since Joe Biden entered the White House.

It took the first 225 years of U.S. history for the U.S. national debt to reach the 6 trillion dollar mark, and now we have added more than 6 trillion dollars to the debt in less than 3 years.

This is what the endgame looks like.

We are in a debt spiral that is totally out of control, and there is no way that this story is going to end well.

And despite the fact that we are endlessly pumping colossal piles of cash into the economy, our economic conditions continue to deteriorate.

On Wednesday, we learned that U.S. job openings have fallen “to the lowest level in more than two years”…

U.S. job openings dropped in November to the lowest level in more than two years, the latest evidence that the Federal Reserve’s interest-rate hike campaign is continuing to cool the labor market.

That is a sign that the economy is getting worse.

And more large companies continue to lay off workers. For example, Xerox just announced that it will be laying off 15 percent of its workforce…

Xerox on Wednesday announced it will cut 15% of its workforce as part of a plan to implement a new organizational structure and operating model.

Xerox, which offers digital printing and document management technologies, had about 20,500 employees as of Dec. 31, 2022, according to a filing with the U.S. Securities and Exchange Commission. Based on this figure, Wednesday’s layoffs will affect about 3,075 employees.

Shares of Xerox closed down more than 12% following the announcement Wednesday.

So what can we do to “get the economy going again”?

Well, we can follow the example of the federal government and borrow and spend even more money.

Of course, much of the nation is already drowning in debt. According to one recent survey, only about half the country will be able to pay off their December credit card balances in full…

Only half of America’s credit card customers believe they can pay off their December balance in full, according to an industry index, signaling a low ebb in “credit card confidence” as the nation emerges from the holidays.

The LendingTree Credit Card Confidence Index, a monthly survey published since 2018 by the personal finance site, dipped to 51% in December, an all-time low.

In a nationally representative survey of 1,514 cardholders, only 51% voiced confidence that they could pay off their card balance this month. In November, the Confidence Index stood at 58%.

Our forefathers handed us the keys to the greatest economic machine in world history.

But that was never enough for us.

We always had to have more, and so we just kept borrowing and spending.

Now the endgame has arrived, and it is going to be excruciatingly painful.

U.S. consumers are drowning in record levels of debt, U.S. corporations are drowning in record levels of debt, state and local governments are drowning in record levels of debt, and the federal government is drowning in record levels of debt.

America’s empire of money was nice while it lasted, but now the jig is up and the collapse that is looming is truly going to be one for the history books.

That’s what the globalists say, you will own nothing and be happy. Except you won’t be happy, you will own nothing. But you’ll be hopping mad because they will have stolen it from you. And you’ll wonder how did they do that? Well, this is how they’re doing it. This is the mechanism. They’ve created a legal mechanism that will stand up in court that you can’t challenge. When they flip the switch, and crater the banking system, we’re all going to lose everything in the bank.

https://www.naturalnews.com/2023-12-18-the-great-taking-how-they-plan-to-steal-everything.html

This is a partial transcript of Brighteon Broadcast News, Dec 18th, 2023, focused on “The Great Taking” documentary by David Webb, which reveals a nefarious plan by central banks to quite literally steal all assets from nearly everyone during the next engineered debt collapse. Find links to the documentary and a downloadable PDF at TheGreatTaking.com.

Hear the full podcast on this when it goes live at this HR Report channel on Brighteon.com.

I really encourage you to watch this documentary The Great Taking by David Webb. If you’re paying attention, then you’ll realize that he’s talking about the creation of this new legal construct called a security entitlement. Now, what this means is that you think that you own your securities, stocks, bonds, bank accounts, whatever debt instruments, you think you own them. But you actually don’t own them. You have been you have been displaced, you’re no longer the owner, you are someone who is entitled to the benefits of this instrument, but you do not own it.

Instead, the ownership is now taken over by essentially these shell corporation organizations that enjoy special protections from the United States government. So when the system collapses, you will own nothing, which is exactly what the globalists are promising.

By the way, when the banks collapse, you will still owe the bank for your home your car business loan. They won’t wipe out your debts, but they will wipe out your assets. Technically, they will seize control over them, and you will become just a creditor to the bank. So if you have a million dollars in the bank, and you think you’re a millionaire, actually, they’re going to take the million dollars and leave you with nothing. But if you have a loan with the bank, you still have to make payments on those loans. So you will end up with no assets, but all your debts, and you will probably be bankrupt.

This is how they’re going to bankrupt people all across the country, which is why it’s called The Great Taking.

The importance of “off-grid” financial assets

This is a strategy that has been constructed by the financial empires to quite literally take possession of virtually all assets currently held by the people of the United States of America. And similar laws have been put in place around the world. So this is why it’s critical to have assets that I call off-grid assets, they need to exist outside the banking system. Number one, it’s critical to get out of debt if you can. I know that some people out there say that debt is your friend and that you should use that to become wealthy and the more debt you have, the more assets you control, and so on. I’ve heard those arguments. That’s not what I follow. You can, of course, decide what’s appropriate for you.

Perhaps if you’re in real estate, maybe debt is your friend when interest rates are low. But then again, debt can quickly become your enemy as rates go higher. But I don’t believe in debt. I’ve been debt-free for a long time. And I do not take loans. I do not ever want to be in debt. Because when you’re in debt, it means they have power over you and it means they can take assets back from you. What we’re finding out in this documentary, The Great Taking is that if you have a home that you ever had a loan on, or if you own a car that you ever had a loan on your title, the fact that it had a lien on it at one time or another may, under certain circumstances, allow the lenders to still claim your property as collateral during a collapse, which means that they could potentially, at least as I understand it, they could come take your house or take your car, even though you’ve paid it off. Because they could claim that it’s collateral on their books, and you are just a “security entitlement receiver,” that you don’t really own it, even though you’re paying it off.

This is what David Webb is describing, in part, in this documentary. Now, I know this is gonna sound completely shocking to most listeners here, especially those of you in finance and taxation and so on, you’re gonna say no, that’s, that’s impossible, that you might think I must be somehow missing the point on this or I’m reaching the wrong conclusion. Well, what I’m saying is, this is what David Webb is describing. And it does contradict normal, financial common sense. It violates all the rules of ownership that we know. But that’s the point of the documentary. David Webb explains that a new system has been put in place that violates all the normal rules of ownership, even in cases of fraud, if a financial institution commits fraud, and they lied, and they cheated, they can still claim your assets as theirs, under certain circumstances.

So watch that documentary to get full details. Of course, check with all your professionals. You know, your professional accountant, your professional real estate investment advisor, your professional Retirement Advisor, your professional dog walker, your professional, whatever, if you have all these professionals, ask all of them. But do your own research, because most people who are professionals in the realm of finance and taxation do not know about this. So do your research and make up your own mind. But what I’m saying is, as a precaution, minimize your exposure to the banking system. Get out of that.

Digital assets can vanish in an instant

I have always said that I do not trust assets held by other parties, where I log in, and they just show me you know, numbers on a screen. Oh, look, you have this many shares of this stock. Yeah, I don’t believe it. I mean, just because it’s on the screen, that doesn’t mean anything. What happens when your brokerage goes out of business? Well, David Webb just answered that question. When the brokerage goes under, they take all your assets, and you become a creditor.

So you thought you owned 1000 shares of Apple, let’s say, and in reality, you don’t. Because you don’t have the shares. They’re not in your possession and your name is not even on them. The brokerage, their name is on the ownership of the shares. They’re the ones who own them. And so when they become insolvent, and then all their assets have to be liquidated through the bankruptcy courts, you know, you might get pennies on the dollar at that point. So I don’t trust dollars in the bank. I don’t trust stocks with an online broker. I don’t trust even treasuries with the US Treasury, Treasury Direct. I don’t trust any of that stuff. You know what I trust? Well, you’ve heard me say it, time and time again, gold and silver and land. And more recently, goldbacks, as well as privacy, crypto, and other assets that hold value even when the system goes down.

Ammunition, garden seeds, diesel, fuel, power tools, things like that. Those are the things that I really trust. And those are the things that I want to have in my self custody or at least under my direct control. If I own gold, I want to take possession of the gold or at least know where it is, or have a way to get to it. I know that’s not a perfect circumstance for everybody. And depending on where you live, your gold might be safer in a vault somewhere. Or if you have a lot of silver, you might want to have it vaulted. Because silver’s kind of bulky and kind of heavy. That’s up to you. But for me, if the system goes down, I want to have direct control over these assets. And apparently, a lot of people agree with me because almost all those assets that I’ve been mentioning, have been going up in value in terms of dollar denominations. Gold has been trending up and silver and also land in many areas of the country.

Some cryptos are rapidly gaining in value

But I was also shocked to learn that one of the privacy cryptocurrencies that we’ve covered at Decentralize TV went up almost 1,000% And that currency is called Beam. I guess it was like two weeks ago or somewhere around that beam shot up from around I don’t know three cents per coin to something like almost 30 cents per coin. Now, it has settled quite a lot since then down to about 10 cents currently. I just checked and apparently I missed the whole thing. And I hold some amount of Beam by the way and I wasn’t paying attention. You know, I was focused on this AI project. But out of the blue, I happen to see Beam pricing. It was like whoa, that’s like 300% higher now than it was a month ago.

That interview by the way, if you want to check it out is on Decentralize.TV look for the interview with the founder of Beam. I like Monero, also, by the way, as a privacy crypto and Monero has gained value, and Bitcoin has gained a lot of value. It’s gone up from around $28,000 a few months ago to now $41,000. And why is that? Why is Bitcoin going up? Why is Monera going up? Why is Beam suddenly skyrocketing? I think it’s because more and more people are realizing the risks in the fiat currency financial system. I think people are dispersing their assets into more redundant vehicles.

People are buying gold and silver. People are buying ammunition. And people are buying privacy crypto, and some people are buying Bitcoin as well. By the way, we have last week, we interviewed Gene, one of the project leaders for Epic Cash. And that interview is coming out. I don’t know probably tomorrow, I think for decentralized TV. Either today or tomorrow, probably tomorrow. So you can check out that interview as well. But anyway, my point is, that people are trying to reduce their risk by getting out of assets that are controlled by the central authorities that David Webb was talking about in his documentary, anything that’s under the control of federal regulators, which includes the FDIC, which controls banking. Any of those banking assets, in my opinion, are at great risk of being confiscated during the debt reset, some people call it the great reset. Some people call it a debt collapse. I don’t know what you want to call it. But it’s pretty clear to me that there’s a day coming, when there will be a deliberate reset of the entire financial system. And in that reset, most of the assets of most Americans will be confiscated.

That’s what the globalists say, you will own nothing and be happy. Except you won’t be happy, you will own nothing. But you’ll be hopping mad because they will have stolen it from you. And you’ll wonder how did they do that? Well, this is how they’re doing it. This is the mechanism. They’ve created a legal mechanism that will stand up in court that you can’t challenge. When they flip the switch, and crater the banking system, we’re all going to lose everything in the bank. I’ve already surrendered to that idea, in a sense, because I have to have a certain amount of operating capital, obviously, you know, to run our platforms and meet payroll and purchase raw materials and whatever. All that money is going to vanish overnight. So I try to minimize that money. Of course, I try to have redundancy and resiliency and backup plans and stay out of debt and all these other things. But you need to be thinking about what happens when they pull the plug on this system.

The coming “cyber attack” narrative to explain away the debt reset

Now it’s possible they could blame it on a cyber attack. That would be a very convenient scapegoat. Blame it on China, blame it on Russia, blame it on aliens, who knows, blame it on hackers. Or even frankly, I think they could blame it on AI cyber attacks, doesn’t even have to be human anymore. They just say, well, an AI system got loose and it hacked all the banks. And now the AI took all your money. It wasn’t us it was the AI robots!

You know, they can say that. And if that showed up in the New York Times, and CNN, frankly, half the country would totally believe it. Oh, yeah, robots stole my money. No wonder I’m broke, you know! It’s also not all fiction. It could happen. But AI robots are probably not going to come to your house and take your gold. And if they tried, you could fight. You know, they’re gonna seize electronic assets. That’s what’s gonna go bye-bye. But everything that’s physical that’s under your control, well, that’s very hard for them to take from you.

And in my opinion, it’s the people who hold the gold that are going to be able to reboot society. They’re going to be the ones that own the future businesses that help launch new currencies. They’re going to be the ones that are position as the new leaders of the entire fiscal economy after the reboot, you’re gonna see millionaires and billionaires become penniless. And then you’re gonna see people who own gold and silver and land become billionaires, I think you’re gonna have a big switch, you know, trading places, it’s going to happen virtually overnight, because who knows how much gold is going to be worth in this collapse environment. I can’t even put a dollar figure on it because the dollar probably won’t exist. It’s, it’s infinite dollars if the dollar goes to zero, you know, division by zero.

So we can’t even properly describe what gold will be worth or silver or hard assets. But I can tell you that fiat currencies will be worth zero or near zero. And your claim on a bank that closed down even if you had a million dollars in the bank, and they they went bankrupt, your claim on that million dollars will be worth, you know, pennies on the dollar, it won’t be worth much at all. This is why I think it’s very much worth your time to look at hard assets.

Hear the full podcast on this when it goes live at this HR Report channel on Brighteon.com.

https://www.shtfplan.com/headline-news/deflation-on-the-way-followed-by-stock-market-crash

by Mac Slavo

Donald Luskin, an economist andTrendMacro CIO said that “deflation is coming” and it will cause a stock market crash. Ahead of the December meeting, Luskin argued the Federal Reserve’s “dangerously high” interest rate hikes are transitory, and that the Fed will make cuts in the first quarter of next year.

“Please, please, please, can we all stop listening to Jay Powell? Please. Mr. Inflation is transitory. He is still so embarrassed about that one. He’s now insisting that his dangerously high interest rates are not transitory. Oh, they will be,” Luskin said according to a report by Fox News. “Inflation is collapsing and he knows it. It’s turning into deflation like I warned last time we talked. There will be rate cuts in Q1.”

Lusking made the comments on “Mornings with Maria,” as he explained his frustration with the Fed’s rate hike campaign and his economic outlook.

The Fed has raised interest rates sharply over the past year, approving 11 rate increases in the hopes of crushing inflation and cooling the economy. In the span of just 16 months, interest rates surged from near zero to above 5%, the fastest pace of tightening since the 1980s.

The Fed voted during meetings in both September and November to hold interest rates steady at a range of 5.25% to 5.5%, the highest level in 22 years. -Fox Business

Luskin claims that the signs are pointing to deflation now as inflation has already hit hard. “We did four back-to-back 75 basis point rate hikes in the middle of last year. That’s never happened before. The last of them was over a year ago. Don’t you think we’d start seeing that right now?” Luskin said.

Investors now see a near 100% chance that Fed officials will hold interest rates steady at their final meeting of the year on December 12-13, according to data from the CME Group’s FedWatch tool, which tracks trading. Other investors also expect the central bank to begin cutting rates in the middle of next year amid signs the economy is cooling.

“In two weeks, the next time CPI reports, it’s going to be the second back-to-back monthly number with a minus sign in front of it. We are at the beginning of the wavefront of outright deflation,” Luskin predicted.

“We are going to have statistical deflation, which I think is a very good thing after the big inflation we’ve had. That doesn’t mean the Fed won’t panic. That doesn’t mean the market won’t panic. So I think, probably sometime late first quarter of next year, second quarter, we’re going to have a severe correction in stocks. It will be a buyable dip.”

In many ways, the modern American Administrative and Deep State, with its “public-private partnerships”, has come to resemble the 17th through 19th century British monarchy, with an entrenched bureaucracy (the permanent administrative state) functionally managed by a largely hereditary elite, surrounded by the concentric status rings of courtiers which comprise the Deep State (in the current embodiment).

https://www.zerohedge.com/geopolitical/malone-psywar-washington-dcs-bureaucracy

TUESDAY, NOV 07, 2023

Authored by Dr. Robert Malone via Substack,

Lack of market force corrections combined with PsyWar propaganda yields unstoppable parasitic growth…

My Dearest American Friends and Colleagues:

Just in case you didn’t notice, since the 1980s we have developed a very big problem which is growing exponentially. The US national debt has become unsustainable.

To a significant extent this debt is enabled by irresponsible printing and injection of fiat currency into the overall US economy by an unaccountable private “Federal Reserve” Bank. Today’s Federal Reserve routinely acts as a willing enabler rather than a check on administrative and deep state spending. The management of the Federal Reserve has become integrated into the interests and culture of the permanent bureaucracy. But that is merely one of many symptoms of a deeper problem.

Many factors drive this explosion of debt, but near the top of the causation list is that the executive branch and its permanent bureaucracy (administrative state + deep state) just does not care. They have no pressing reasons to care. They have developed a whole special economic logic to justify and rationalize not caring, called Modern Monetary Theory (MMT).

Functionally, unlike either industry (market forces) or the military (failed wars), there are no external forces currently limiting the expansion of the dysfunctional, counterproductive and (frankly) parasitic behavior of today’s Executive branch. Legislative branch oversight has been emasculated by consent with lobbyists collectively clamping down the Burdizzo, and in 1984 the Judicial branch conceded its authority to serve as a functional check on Executive/administrative branch arrogance via the Supreme Court Chevron Deference decision. And like the Federal Reserve, the informal “fourth estate” (corporate media), which historically provided a separate and semi-autonomous oversight function, has also been captured by this permanent bureaucracy.

The administrative and deep state has been so successful in capturing and manipulating media and related communication (largely via CIA, FBI, CISA and intelligence community infiltration) that they are able to seamlessly deploy advanced modern propaganda, PsyWar technologies and financial giveaways to control all narratives and information which might otherwise cause the majority of the electorate to check their actions, and in this way they completely avoid accountability. The CIA, FBI, CISA and intelligence community have become enablers of administrative and deep state excesses and overreach. With this corrupted information ecosystem, there cannot be any accountability of the administrative and deep state. In cooperation with a variety of corporate and NGO partners via “public-private partnerships”, the executive branch has completely captured and co-opted all oversight mechanisms which could enable or enforce checks and balances. The “ballot box” is well on its way to being a mere inconvenience, because for the majority of voters the synthetic false reality projected by captured media is the only political “reality” they encounter.

This is how modern nation-states abruptly collapse. As one recent example, recall the history of the USSR and most of the former communist Eastern European states. Modern nation-states fail by suffocating under the weight of bloated unaccountable bureaucracies whose primary objectives are to serve and sustain themselves rather than to promote and defend the general welfare and security of the citizenry. The social contract is stomped into dust by the boot of an uncontrollably arrogant, authoritarian, self-serving bureaucracy.

To what purpose are powers limited, and to what purpose is that limitation committed to writing, if these limits may, at any time, be passed by those intended to be restrained?

-John Marshall, Chief justice of the United States from 1801 to 1835

To illustrate my point with one example of the current situation, please consider the following from “Heard Around the Hill”. This is a publication of the Council on National Policy, which has provided a snapshot of the current state of the Federal Budget stalemate between the Legislative branch – constitutionally tasked with managing the federal budget and funding the government, and the Executive branch (and it’s permanent administrative bureaucracy) – tasked with administering that budget.

House Republicans passed a plan to address the nation’s debt ceiling Wednesday, tying the increase to desperately-needed spending limits and reforms.

The package includes:

- Limiting future spending to FY22 levels

- Reclaiming unspent COVID money

- Defunding 87,000 new IRS agents

- Implementing work requirements for government assistance programs

The White House refused to negotiate, insisting Congress give them a blank check for future spending and betting that proposed reforms could not garner enough votes in the House.

Even Democrats have been critical of Biden’s refusal to negotiate. Senator Manchin described the approach as a “deficiency of leadership.” House Members have also disapproved of the tactic.

“A Down Payment On Fiscal Sanity” is how economist and former Assistant Treasury Secretary Mike Faulkender detailed the Republican plan.

In discussing the current state of US Federal government, these terms “Administrative State” and “Deep State” are often tossed about as if they are one and the same, but that is most definitely not the case. As described by Kash Patel, the Deep State is a type of shadow governance made up of informal, extra-constitutional, secret and unauthorized networks of power operating independently of a nation state’s duly elected political leadership, acting in pursuit of agendas and goals which are separate from the interests of the citizenry.

Administrative State is a term used to describe the phenomenon of executive branch administrative agencies which exercise bureaucratic power to create, adjudicate, and enforce their own rules. The administrative state abuses congressional non-delegation, judicial deference, executive control of agencies, procedural rights, and agency dynamics to assert control over and above both republic and constitutional principles.

Another related term often used to describe the modern American bureaucratic state is “Leviathan”, a word with biblical origins repurposed as the title of Thomas Hobbes’ monarchist 1651 book which advocates a strong centralized government. Hobbes argues that civil peace and social unity can be best achieved through the establishment of a commonwealth via a social contract. Hobbes’ ideal commonwealth is ruled by a singular sovereign power responsible for protecting the security of the commonwealth, while being granted absolute authority to ensure the common defense.\

In many ways, the modern American Administrative and Deep State, with its “public-private partnerships”, has come to resemble the 17th through 19th century British monarchy, with an entrenched bureaucracy (the permanent administrative state) functionally managed by a largely hereditary elite, surrounded by the concentric status rings of courtiers which comprise the Deep State (in the current embodiment). Within the growing hereditary ruling American oligarchy there is some degree of turnover and palace intrigue, as the fortunes of some wane while others rise. As with the rise of the British bourgeoisie and mixing of gentry with financially successful upper middle castes, this often reflects broader financial and technological trends within the overall geo-political and geo-economic context in which a globalized oligarchy competes.

The obvious irony being that this type of system was precisely what the American Revolution was intended to overturn, and precisely what the US Constitution was written to prevent.

And above all of this, we have now added a transcendently powerful new capability to the Leviathan of old. The rise of the CIA and its “Mockingbird/Mighty Wurlitzer” infiltration of both media and academia, the FBI and its politically weaponized COINTELPRO-type surveillance, infiltration and disruption capabilities, the DoD and its PsyOps/PsyWar capabilities designed for offshore conflicts but turned against domestic citizenry to support executive branch-defined “crisis” management, and the explosive growth of a new censorship-industrial complex has yielded a “Leviathan” with reality-bending information control capabilities the likes of which the historic British monarchy could only dream of. Propaganda has come a long way from the days of Edward Bernays’ seminal 1928 book by the same name.

The Washington DC-based Administrative/Deep State has emerged as a separate entity unto itself, with its own culture, purpose, privileges and prerogatives. A key characteristic of this separate cultural phenomenon and mindset- often geographically referred to as the “inside the beltway” set (referring to the I 495 freeway loop encircling DC and environs)- is a focus on self-preservation and personal advancement, rather than on achieving a mission, producing a deliverable, or serving the needs of outside-the-beltway flyover state serfdom.

Imperial DC beltway denizens form an incestuous culture, much like any historic imperial court. Passive-aggressive “slow walking” of initiatives has been refined to a fine art. Sexual favors are routinely exchanged to seal short-term alliances, both within agencies and between contractors and “Govies”. Nuances of administrative regulations are weaponized to enable petty counterproductive one-upmanship. “Beltway Bandit” corporations, lobbyists (registered and unregistered) and “think tanks” cultivate, collect and support Deep State “swamp monsters” when the political wing they are allied with is out of power for a period, anticipating that these courtiers will be rotated back in with the next political shift or Executive branch “change” in leadership. And all are tied together in a revolving maypole dance. Together, they collectively weave a Uniparty in which the commonalities of shared commitment to advancing the interests of the Administrative/Deep State court are far more important and lasting than any inconvenient superficial narrative about serving the interests of the general electorate and citizenry. In this beltway culture, actually solving national problems takes a back bench to the pageantry and Machiavellian machinations of the elite courtiers and their allies.

No wonder the general populace often feels that their votes for elected Federal officials are irrelevant. Because they are, in fact, increasingly irrelevant. And as if that were not bad enough, the permanent administrative state considers elected and politically appointed officials to be “temporary employees”. The shadowy members of the unaccountable Senior Executive Service (SES) are the ones that actually administer the government.

But with the advance of PsyWar capabilities, bolstered by advances in modern psychology, and combined with algorithmic control, censorship, and manipulation of all information, Deep State beltway denizens have been able to achieve a propaganda capability which rivals the Atomic Bomb in its political implications.

These actors are now able to decouple their activities from objective truth. There can never be any accountability or consequences for mismanagement or misdeeds when they are able to effectively control all information and communication. Objective reality has become a theoretical post-modernist, surrealist construct, able to be contorted, moulded and enforced to comport with any synthetic version of reality which best supports Administrative State, SES and Deep State objectives. Corporate and social media lapdogs (rapidly becoming dominant via alliances with globalized investment funds), are bolstered and legitimized by coopted academia. Together they often act under the strong influence of Administrative State “intelligence” agencies and Deep State actors, and stand ever ready to create, control, propagate, and reinforce whatever narrative is needed.

Desire to achieve this sort of reality-bending groupthink or mass psychosis has been a common feature of bureaucracies, aristocracies, monarchies and oligarchies for as long as historical records have been kept. But what is different now is the power and penetration of modern digital algorithmic control mechanisms. We now witness creation of a lobotomized servant caste which enables an administrative bureaucracy nirvana of complete lack of accountability is now within reach. What could possibly go wrong?

I believe that a short answer is “paradigm shift”. This type of cognitive landscape, in which a synthetic reality is preserved and maintained despite increasing divergence from objective reality, is a setup for abrupt introduction of more adaptive alternatives. Examples of synthesized false realities include an unsustainable federal debt, a collapsing “safe and effective” COVID vaccine narrative, and the intrinsic contradictions of human activity-driven carbon dioxide levels representing a global existential crisis. Actively fabricated false realities create a situation where current governmental solutions drift further and further from optimal.

At some point, an abrupt disruption in perception, power, global finance or available technology will occur – a paradigm shift. And when a system, technical or political, has been prevented by externals from adapting to changing conditions (such as happens with propaganda), then a crisis can trigger catastrophic realignment of divergent synthetic and objective reality. In politics, these “earthquake” moments reflect abrupt resolution of shifting internal forces which have built up tension along a fault line, and often result in either revolutions or catastrophic failures of economies and civilizations.

Functionally, the US Government is now managed by disconnected Senior Executive Service (SES) “leadership”, acting in harmony with Administrative and Deep State castes, massive transnational financial institutions, public-private partnerships, corporate lobbyists and globalist non-governmental organizations such as the UN, WHO, WEF and Gates foundation. This supra-constitutional alignment has enabled permanent Administrative and Deep State “management” of an out-of-control federal budget which supports a grotesque obsession with their maypole dance, court drama, one-upmanship, and Machiavellian machinations. And all who object are censored, subjected to character assassination and labelled fringe outliers by captured media.

Rather than solving the missions and problems which plague the electorate that they currently parasitize, these erstwhile public servants have removed any ability of citizenry and electorate to provide the oversight, control and correction function originally designed into the US Constitution by those with lifelong experience in dealing with an earlier Leviathan. One that was also characterized by arbitrary and capricious administrative authoritarianism. And in the current embodiment we now have amazingly powerful psychological tools placed in the hands of venal, self-serving, immature and all too often sociopathic individuals seeking self-gratification.

Indeed, what can possibly go wrong?

Abrupt, catastrophic economic and/or military collapse, that’s what.

How many wars has the USA lost since WW II? And now this amazingly expensive and corrupt Ukrainian foreign adventure is deconstructing itself. Which (mis) adventure seems to have mostly worked to strengthen and hone Russian military might while depleting and fracturing NATO unity and capabilities. Biden sought to drain and exhaust Putin, thereby yielding Russian regime change. In an amazing feat of geopolitical jiu-jitsu, the precise opposite may well come to pass.

And then we have the obscenely bungled public health and financial responses to the COVID crisis. And growing awareness that the “climate crisis” has been synthesized and weaponized to advance a variety of geopolitical power, control and financial objectives.

This level of massive Administrative and Deep State mismanagement is not sustainable, even with US economic and natural resource muscle.

History and archaeology is littered with the bones of civilizations and bureaucracies which became inwardly focused and lost track of their function and purpose. I would love to believe in a fairy tale world in which modest modifications in administrative agency guidelines and practices could result in a more functional ruling bureaucracy. But I am too old for fairy tales, and have myself spent too many years in the bowels of the Federal administrative state.

I fear that the dysfunctional and fundamentally corrupt DC Beltway culture will not change until we have a massive paradigm shift of some sort or another. Resolving these structural problems will require a major correction. It could occur at the ballot box, but the power of the intelligence community/censorship-industrial complex to distort reality to protect itself may have already reached a stage where this cannot happen. However, the debt, the massive unsustainable debt, combined with the insatiable hunger of the Administrative and Deep State working cooperatively with the industrial masters of forever war and “biodefense” may soon trigger a global paradigm shift in power and finance.

And if that happens, I can only hope that I have enough guns, ammo, farm infrastructure and a well-developed network of like minded friends to ride out the following storm.

But in such a brave new world, getting diesel for trucks and tractors will definitely be a problem. Probably time to dust off my equine teamster skills and train some horses to pull.

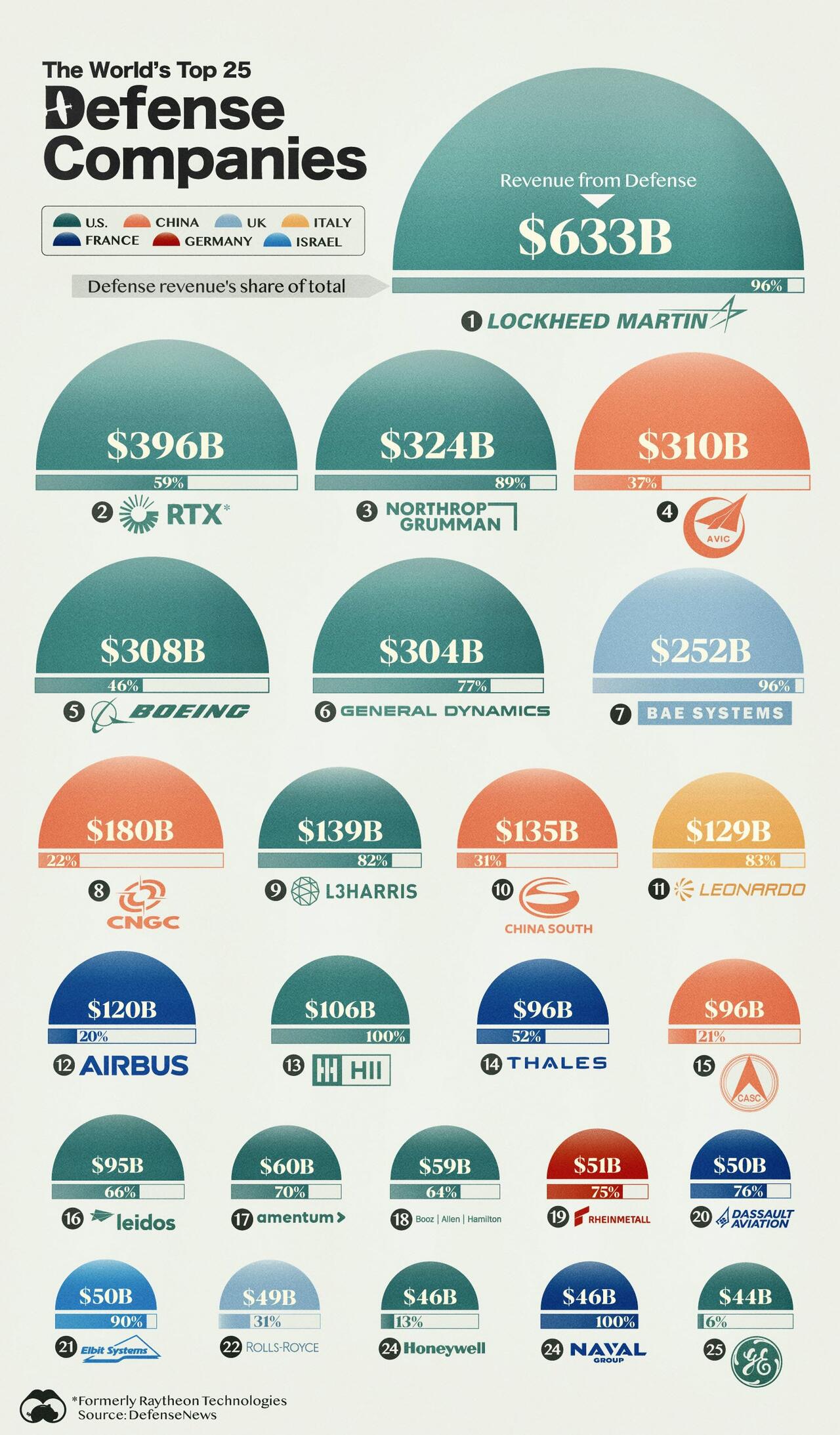

“It is possibly the oldest, easily the most profitable, surely the most vicious. It is the only one international in scope. It is the only one in which the profits are reckoned in dollars and the losses in lives.“

https://www.zerohedge.com/military/war-racket-these-25-defense-companies

BY TYLER DURDEN

SUNDAY, OCT 29, 2023

Retired US Marine Corps Major General Smedley Butler said it first and said it best: “War is a racket. It always has been…”

But what often goes unsaid is his next sentences:

“It is possibly the oldest, easily the most profitable, surely the most vicious. It is the only one international in scope. It is the only one in which the profits are reckoned in dollars and the losses in lives.“

And indeed, every year, the world’s most powerful countries spend billions of dollars on so-called ‘defense’.

But where does this money actually flow?

To gain insight, Visual Capitalist’s Marcu Lu and Bhabna Banerjee ranked the world’s top 25 defense companies by 2022 revenues, using data from Defense News.

Note that their graphic shows each company’s revenues from defense, and not total revenues. This is because many companies such as Boeing also generate revenue from non-defense related industries and sectors.

Data and Country Highlights

The data we used to create this graphic is listed in the table below.

| Company | Revenues from Defense (USD billions) | Defense share of total revenue (%) |

|---|---|---|

| 🇺🇸 Lockheed Martin | $633 | 96% |

| 🇺🇸 RTX Corp (formerly Raytheon Technologies) | $396 | 59% |

| 🇺🇸 Northrop Grumman | $324 | 89% |

| 🇨🇳 Aviation Industry Corporation of China | $310 | 37% |

| 🇺🇸 Boeing | $308 | 46% |

| 🇺🇸 General Dynamics | $304 | 77% |

| 🇬🇧 BAE Systems | $252 | 96% |

| 🇨🇳 China North Industries Group | $180 | 22% |

| 🇺🇸 L3Harris Technologies | $139 | 82% |

| 🇨🇳 China South Industries Group | $135 | 31% |

| 🇮🇹 Leonardo | $129 | 83% |

| 🇳🇱/🇫🇷 Airbus | $120 | 20% |

| 🇺🇸 HII | $106 | 100% |

| 🇫🇷 Thales | $96 | 52% |

| 🇨🇳 China Aerospace Science and Technology Corporation | $96 | 21% |

| 🇺🇸 Leidos | $95 | 66% |

| 🇺🇸 Amentum | $60 | 70% |

| 🇺🇸 Booz Allen Hamilton | $59 | 64% |

| 🇩🇪 Rheinmetall AG | $51 | 75% |

| 🇫🇷 Dassault Aviation | $50 | 76% |

| 🇮🇱 Elbit Systems | $50 | 90% |

| 🇬🇧 Rolls-Royce | $49 | 31% |

| 🇺🇸 Honeywell | $46 | 13% |

| 🇫🇷 Naval Group | $46 | 100% |

| 🇺🇸 General Electric | $44 | 6% |

The U.S. and China are the most represented countries on this list, with 12 and four respective companies in the top 25.

Country Highlights: U.S.

The U.S. consistently has the world’s largest military budget, so it’s no surprise that American companies dominate this ranking. Here are some interesting facts about the top three:

Lockheed Martin

- Formed in 1995 by the merger of Lockheed Corporation and Martin Marietta

- While primarily known for producing advanced fighter jets like the F-35, the company is also working with NASA on the Orion spacecraft

RTX (formerly Raytheon Technologies)

- Raytheon produces a wide range of military equipment, including the Javelin portable anti-tank missile system.

- According to CSIS, the U.S. has supplied 7,000 Javelins to Ukraine, equal to roughly one-third of its stock.

Northrop Grumman

- Formed in 1994 by the merger of Northrop and Grumman Aerospace, this company is known for developing the B-2 stealth bomber.

- In August 2023, the company opened an office in Taiwan to “accelerate access to the company’s technologies”.

Country Highlights: China

China’s top three companies in this ranking are all state-owned enterprises.

Aviation Industry Corporation of China (AVIC)

- AVIC is China’s largest aerospace and defense company, also ranking 150th in the Fortune Global 500 (2023).

- Chengdu Aerospace Corporation, a subsidiary of AVIC, produces China’s first operational stealth fighter, the J-20.

China North Industries Group (CNIG)

- CNIG does business internationally under the name Norinco Group.

- In 2003, Norinco was sanctioned by the Bush administration for allegedly supplying Iran with missile technologies.

China South Industries Group (CSIG)

- CSIG produces military vehicles, ammunitions, and other equipment.

- The company also owns Changan Automobile, a major car brand in China and one of the world’s largest EV producers.

Other Highlights

Two European companies on this list that aren’t typically associated with the defense industry are Airbus and Rolls-Royce.

Airbus is one of the world’s largest producers of commercial airliners, and is widely used by major carriers alongside offerings from Boeing. When it comes to defense, Airbus produces a variety of military drones, fighters, and transports.

On the other hand, Rolls-Royce is a major supplier of aircraft and naval engines, and designs the nuclear propulsion systems for the UK’s submarine fleet.

It actually has no affiliation with Rolls-Royce Motor Cars, which is currently a subsidiary of BMW. The original company ran into financial difficulties in the 1970s, which led to the separation of the car and aero-engine businesses.

The nation officially hit its $31.4 trillion debt ceiling in January

https://www.rt.com/business/575636-us-debt-default-warning/

May 2, 2023

© Getty Images / WOWstockfootage

US Treasury Secretary Janet Yellen warned on Monday that the federal government could run short of cash to pay its bills as soon as next month without a debt limit increase.

“After reviewing recent federal tax receipts, our best estimate is that we will be unable to continue to satisfy all of the government’s obligations by early June, and potentially as early as June 1, if Congress does not raise or suspend the debt limit before that time,” Yellen wrote in a letter to House and Senate leaders.

She urged congressional leaders “to protect the full faith and credit of the United States by acting as soon as possible.”

“We have learned from past debt limit impasses that waiting until the last minute to suspend or increase the debt limit can cause serious harm to business and consumer confidence, raise short-term borrowing costs for taxpayers, and negatively impact the credit rating of the United States,” Yellen wrote.

“If Congress fails to increase the debt limit, it would cause severe hardship to American families, harm our global leadership position, and raise questions about our ability to defend our national security interests,” she cautioned.

The Congressional Budget Office (CBO) also updated its forecast on Monday, warning there was a “significantly greater risk that the Treasury will run out of funds in early June” because of weaker-than-expected tax collections. The CBO had originally projected that a default could happen between July and September.

READ MORE: US debt default a matter of time – Musk

The warnings come after a months-long standstill in talks on the matter between the White House and Republicans in Congress.

Yellen has been voicing alarm since January, when the United States hit its $31.4 trillion debt ceiling. At the time she notified Congress that the Treasury had begun resorting to “extraordinary measures” to avoid a federal government default.

On Monday, President Joe Biden called all four congressional leaders and invited them to a May 9 meeting on the issue.

In the next few years, the financial system will crash under its own weight in spite of and also due to the coming biggest money-printing avalanche that the world has ever experienced.

Nixon’s closing of the gold window in 1971 was the signal that this currency system was going to end like all currency systems in history. And for the ones who haven’t studied the history of money, let me tell you that NO FIAT MONEY HAS EVER SURVIVED IN HISTORY IN ITS ORIGINAL FORM. So with all money going to ZERO, it has never been a question of if but only of when the dollar-based currency system would die.

https://www.sott.net/article/479008-The-Everything-Collapse

Egon von Greyerz

Gold Switzerland

Sun, 02 Apr 2023

Sadly, gold is now on its way to heights which are unthinkable for most people.

To all the people who have asked me over the years why gold doesn’t go up, I have replied:

“Don’t wish for gold to go up substantially for when it does, your quality of life will deteriorate remarkably.”

And we are now at the point in the world when this is likely to happen.

Let me be clear, now is the time to protect whatever assets you have in order to avoid the total asset destruction that is coming next. More about this later in this article.

THE FINANCIAL SYSTEM WILL NOT SURVIVE

I came to the conclusion early in this century that a sick financial system was not going to survive the infestation of vermin in the form of debt that started just over 50 years ago.

Nixon’s closing of the gold window in 1971 was the signal that this currency system was going to end like all currency systems in history. And for the ones who haven’t studied the history of money, let me tell you that NO FIAT MONEY HAS EVER SURVIVED IN HISTORY IN ITS ORIGINAL FORM. So with all money going to ZERO, it has never been a question of if but only of when the dollar-based currency system would die.

Dalai Lama said:

“If there is a solution to a problem, there is no need to worry.

And if there is no solution, there is no need to worry”

But in this case, my view is THAT WE REALLY NEED TO WORRY.

So sadly, his wisdom doesn’t apply to the global problem that the world is now facing.

IS THE UKRAINE WAR COMING TO AN END

In early January this year I wrote an article called “OMINOUS MILITARY & FINANCIAL NUCLEAR THREATS COULD ERUPT IN 2023.”

I have covered the threat of a major war in many articles in the last 12 months for example “Will nuclear war, debt collapse or energy depletion finish the world“

Although it is too early to be really optimistic, it now looks like my prediction that Russia will never lose this war is getting closer.

Ukraine is making the Battle of Bakhmut into their Stalingrad last stand (WWII 1943).

Ukraine has committed the majority of their remaining forces to win this battle against Russia. If they lose in Bakhmut, even Zelensky believes that this could be the end for Ukraine.

Here is the Associated Press (AP) article in which Zelensky is hinting that Ukraine could lose this war –

“Ukraine’s Zelensky: Any Russian victory could be perilous.”

If Bakhmut fell to Russian forces, Putin would “sell this victory to the West, to his society, to China to Iran” Zelensky said in the AP interview.

“If he will feel some blood – smell that we are weak – he will push, push, push!”

Scott Ritter, the former intelligence officer and UN weapons’ inspector just gave this interview in which he believes that Ukraine is on the point of losing the war:

THE END OF US HEGEMONY

At the beginning of the Ukraine conflict, I and some others made the analogy with the Cuban Missile Crisis in 1962 (which I remember well) when Kennedy gave an ultimatum to Khrushchev to withdraw the nuclear missiles pointing towards the US or face war.

In the same way as with Cuba, Russia was never going to accept Ukraine becoming a Nato country. But sadly the US Neocons have seen this conflict as the last chance to save the US military, political and economic hegemony from total collapse. Defeating Russia was the last stand for the US. But it now looks like they will fail which seals the fate of the US empire.

The US neocons forced a much too willing Europe to not only agree to the sanctions against Russia but also make direct contributions to the war both with money and equipment.

This fatal mistake by Europe and especially Germany is totally crushing the European economy. But what the US neocons never understood is that the US sanctions would affect the whole world and in particular, the debt-infested US and the West.

At the end of an economic era, unexpected events take place which will seal the fate of a crumbling empire.

THE END OF THE CENTRAL BANKER

The script for the first 22+ years of the 2000s couldn’t be more perfect as the final glutinous feast of Gargantua The Central Banker. (Gargantua – book by Rabelais 1543)

Central bankers have been the principal creators of the current crisis which had its beginnings over 100 years ago.

Significant events in the 2000s created by fallacious Central Bank policies:

- 2000-2 Market collapse: Tech stocks down 80%

- 2006-8 Subprime banking crisis: Dow down 54%, massive money printing

- 2009-21 Stocks & asset markets exploding: Dow up 6X, Nasdaq up 16X

- 2006-20 Manipulation of rates: US 10yr treasury down from 5.4% to 0.5%

- 2000-23 US Debt explosion: Up 3.5X from $27t in 2000 to $95t in 2023

- 2000-23 Global debt explosion: Up 3X from $100t in 2000 to $300t in 2023

- 2020-23 Real inflation US EU: Up from 0% in 2020 to 10%+ in 2023

The extreme moves and volatility exemplified in the table above have nothing to do with free markets. They are the manifest consequences of shameless manipulation of markets and market conditions by Central Banks. Such extreme moves could never happen if markets followed nature’s laws and the laws of supply and demand.

For example, in an unmanipulated market, it would be totally impossible for credit to expand exponentially and interest rates to remain at zero. The basic principle of supply and demand would force the cost of money up when demand for credit expands. And if there was no demand, the cost of money would obviously come down to the level where demand resumes.

If markets were allowed to follow the natural rhythm of nature, they would be self-correcting without extreme tops and bottoms.

This is so basic that a 7-year-old would understand it. But the Central Bankers choose to ignore it.

The obvious consequence of markets flowing naturally without intervention would mean that we could get rid of Central Bankers. How wonderful! No Central Banks, No Manipulation and No Extremes in the economy or markets.

Sadly, such simple solutions are the exception in history with greed and power driving man rather than reason and logic.

The bankers clearly knew what they needed to do when they met on Jekyll Island in 1910 in order to control the US and the global monetary system. At this meeting, they schemed to create the Fed in 1913 and followed the axiom of Mayer Amschel Rothschild a German banker in the late 1700s: “Let me issue and control a nation’s money and I care not who writes the laws.”

From Amschel Rothschild to Jekyll Island to Nixon closing the gold window in 1971, the Central bankers and bankers have successfully taken control of issuing exponentially larger amounts of money and debt for their own benefit as well as for a very small elite who could take advantage.

Having created a structure that was above the law as Amschel said, they have so far been in total control of their own destiny with governments being dictated to by the central bankers and bankers. Thus in 2008, the Fed and a number of virtually bankrupt banks, including JP Morgan, Goldman, Morgan Stanley, Bank of America, Barclays etc dictated their own rescue terms to the US and other governments.

But we must remember that 2006-9 was just a rehearsal. The finale is starting now. The debt which has built up has now reached levels which means the financial system is now too big to survive.

Three US banks and one Swiss went under 2 weeks ago although two of the four were rescued temporarily at a high cost. The Swiss government could not afford to let Credit Suisse go under and is supporting the UBS takeover of the Credit Suisse at a potential extraordinary cost of CHF 209 billion.

Central banks are on standby to stop the next bank run. Many expected Deutsche Bank to be next. Governments will stop major banks from going under for as long as they can, to stop global contagion. But they will of course fail.

The FDIC (Federal Deposit Insurance Corporation) currently has a capital of $128 billion dollars to support a total of $18 trillion deposits. So with 0.7% cover, it is guaranteed that the US government will soon need to step in as the next lot of US banks fail. Same in Europe where most EU banks and the ECB are in terrible shape.

Total central bank assets are $ 25 trillion which is less than 10% of global debt before derivatives. Default rates in coming years are likely to exceed 50% which means much more money printing to come.

ALL ASSETS ARE PRICED AT THE MARGIN – PROTECT YOURSELVES

As the current asset bubbles are coming to an end, the exit doors will be totally blocked by panicking sellers.

All assets are priced at the margin and even more so since the current asset bubbles have been created by the most gigantic debt bonanza. To take an extreme example, if there is one seller and no buyer in the housing market, the price of all houses will go to zero. The same is true for the stock market.

But as investors run for the exit, most will not get through since there will at some point be no buyers at any price.

This is how the price of stocks, bonds or property can go down by 75% to 100% in real terms. Some market observers say that this has never happened in history so it won’t happen today either. Yes, of course, I can be wrong, but what we must remember is that nor have we ever in history had a global debt and asset bubble of this magnitude. So we are in unchartered waters and conventional wisdom doesn’t apply and is just conventional without any wisdom.

In any case, investors shouldn’t worry how much their assets could decline. Instead, they should worry about protecting themselves against the risk of this happening.

Firstly investors should go as liquid as possible. Secondly, debts must be repaid. Nobody will want the bank to take their assets at a bargain price.

Short-term government bonds could offer adequate protection. But medium and long term, governments will at best destroy the value of the currency and at worst also default.

Tangible assets are undervalued and a good investment to own.

Physical gold and silver held outside the banking system is the ultimate protection just as in any crisis.

It is absolutely critical to buy gold and silver now before investors panic into these metals. There is very little gold and silver available to buy. Currently, all production is absorbed and any increase in demand cannot be met by increased supply but only by much higher prices.

But remember that gold and silver are also priced at the margin, so as demand increases, we could reach a situation when there is no silver or gold available at any price.

So my very strong advice is not to wait for the herd since you then are likely to be left with no silver or gold and no protection.

But in the end, as I have stressed, the $2 quadrillion debt and derivative liabilities, cannot be saved.

In the next few years, the financial system will crash under its own weight in spite of and also due to the coming biggest money-printing avalanche that the world has ever experienced.

Did you think that the Federal Reserve was just going to stand by and watch the U.S. banking system completely collapse? In response to the stunning failures of Silicon Valley Bank and Signature Bank, the Federal Reserve announced a rescue plan on Sunday evening that is going to radically change banking in America forever. All deposits at Silicon Valley Bank and Signature Bank will be fully guaranteed and will be available on Monday.

March 13, 2023

Did you think that the Federal Reserve was just going to stand by and watch the U.S. banking system completely collapse? In response to the stunning failures of Silicon Valley Bank and Signature Bank, the Federal Reserve announced a rescue plan on Sunday evening that is going to radically change banking in America forever. All deposits at Silicon Valley Bank and Signature Bank will be fully guaranteed and will be available on Monday. Of course the Federal Reserve can’t just make an exception for these two banks. If they are going to do this for them, that means that they are going to have to do it for everyone else too. So what this means is that from this point forward the Federal Reserve is essentially promising to guarantee every bank account in America. Considering the fact that more than 19 trillion dollars is deposited with U.S. banks, that is quite a promise to make.

I want to show you that I am not exaggerating one bit. The following is the announcement about this new plan that was just posted on the official website of the Federal Reserve…

To support American businesses and households, the Federal Reserve Board on Sunday announced it will make available additional funding to eligible depository institutions to help assure banks have the ability to meet the needs of all their depositors. This action will bolster the capacity of the banking system to safeguard deposits and ensure the ongoing provision of money and credit to the economy.

The Federal Reserve is prepared to address any liquidity pressures that may arise.

The additional funding will be made available through the creation of a new Bank Term Funding Program (BTFP), offering loans of up to one year in length to banks, savings associations, credit unions, and other eligible depository institutions pledging U.S. Treasuries, agency debt and mortgage-backed securities, and other qualifying assets as collateral. These assets will be valued at par. The BTFP will be an additional source of liquidity against high-quality securities, eliminating an institution’s need to quickly sell those securities in times of stress.

With approval of the Treasury Secretary, the Department of the Treasury will make available up to $25 billion from the Exchange Stabilization Fund as a backstop for the BTFP. The Federal Reserve does not anticipate that it will be necessary to draw on these backstop funds.

After receiving a recommendation from the boards of the Federal Deposit Insurance Corporation (FDIC) and the Federal Reserve, Treasury Secretary Yellen, after consultation with the President, approved actions to enable the FDIC to complete its resolutions of Silicon Valley Bank and Signature Bank in a manner that fully protects all depositors, both insured and uninsured. These actions will reduce stress across the financial system, support financial stability and minimize any impact on businesses, households, taxpayers, and the broader economy.

The Board is carefully monitoring developments in financial markets. The capital and liquidity positions of the U.S. banking system are strong and the U.S. financial system is resilient.

Depository institutions may obtain liquidity against a wide range of collateral through the discount window, which remains open and available. In addition, the discount window will apply the same margins used for the securities eligible for the BTFP, further increasing lendable value at the window.

The Board is closely monitoring conditions across the financial system and is prepared to use its full range of tools to support households and businesses, and will take additional steps as appropriate.

Please don’t just skim those paragraphs.

Take the time to read them in detail, because what the Fed just did literally changes everything.

From now on, nobody will have to worry that their bank will fail, and the Fed has decided to completely end the war against inflation.

If the technical language confuses you, here is Zero Hedge’s translation…

Translation: the Fed’s hiking cycle is dead and buried, and here comes the next round of massive liquidity injections. It also means that the Fed, Treasury and FDIC have just experienced the most devastating humiliation in recent history – just 4 days ago Powell was telling Congress he could hike 50bps and here we are now using taxpayer funds to bail out banks that have collapsed because they couldn’t even handle 4.75% and somehow the Fed has no idea!

That analysis is right on the money.

I warned that our system could not handle higher interest rates, and higher rates were directly related to the collapse of Silicon Valley Bank.

So there won’t be any more rate hikes.

In fact, I wouldn’t be surprised at all if the Fed started cutting rates very soon.

In addition, all of the fresh money that the Fed will be injecting into the financial system now will be highly inflationary.

We are being told that the Fed’s plan won’t cost taxpayers a dime, but the truth is that inflation is a tax on all of us.

So the financial community may be praising this “extraordinary intervention” by the Fed, but there will inevitably be a very high price to pay for spraying money around so recklessly.

But what other choice did the Fed have?

As I have repeatedly warned my readers, our fundamentally flawed system simply cannot survive without artificial support.

And as Bill Ackman has noted, if the Fed had just stood by and done nothing we would have been facing a nightmare scenario as early as next week…

Over the past several days, we really did come to the brink of the abyss.

But now the Federal Reserve has come charging to the rescue and so everything is okay, right?

I wish that was actually true.

As a result of the Fed’s reckless rate hiking strategy, U.S. banks are now sitting on 620 billion dollars of unrealized losses.

That is “billion” with a “b”, and that is a ticking time bomb that is not going to go away any time soon.

Meanwhile, the housing bubble is imploding, we are heading into the worst commercial real estate crisis in all of U.S. history, and now faith in the U.S. banking system has been greatly shaken.

This crisis is not even close to over.

And every time there is a new eruption somewhere, the Fed will try to put the flames out with generous injections of fresh liquidity.

Virtually everyone applauds when the Fed starts spraying money around, but by now all of us should realize that this story is not going to have a happy ending.

The coming Central Bank Digital Currency prison is truly global in nature, being implemented in nearly every country in the world.

Global Research, February 05, 2023

LifeSite 16 May 2022

Way back in 2017 I created a country-by-country guide to the biometric ID control grid that was coming into view even then. In that editorial I noted that “it doesn’t take a Nostradamus to understand where this is all heading: From the cashless society and the biometric ID grid to the cashless biometric grid.”

Well, here we are. It’s 2022 and the merger of the cashless society and the biometric ID grid is nearing completion. In fact, the current iteration of this control grid agenda is even worse than predicted. Now known as Central Bank Digital Currency, or CBDC, this programmable digital money offers the banksters numerous options, including the ability to combine the cashless society with the biometric ID grid and even a social credit system. If and when CBDCs replace other payment methods, the banksters’ control over society will be unprecedented.

But however closely you might be following the drive toward the CBDC dystopia, you might be missing the forest for the trees. Although each country’s central bankers talk as if they have come up with the idea for a digital currency all by themselves and that there is no international coordination behind the CBDC agenda, nothing could be further from the truth. In fact, as a recent Bank for International Settlements report indicates, 90% of central banks around the world are currently studying the feasibility of issuing their own CBDC.

In the past, I have warned about the coming CBDC nightmare and talked about the numerous ways we can start taking the monetary power back into our own hands.

Today, I am going to drive home the point that the coming CBDC prison is truly global in nature by demonstrating that it is not just being put into place in one or two totalitarian countries, but nearly every country in the world.

Only when we recognize how dire the situation is can we hope to motivate communities to implement the survival currencies that will see us through the controlled demolition of the existing monetary order.

Australia

The Reserve Bank of Australia (RBA) has been exploring the possibility of an Australian Central Bank Digital Currency since at least 2019, when its “Innovation Lab” drafted a Submission to the Senate Select Committee on Financial Technology and Regulatory Technology, which states that “the Bank is conducting research on the technological and policy implications of a wholesale CBDC.”

It made good on this threat in November 2020 with the announcement of a partnership between the RBA and Commonwealth Bank, National Australia Bank, Perpetual, and ConsenSys Software to “explore the potential use and implications of a wholesale form of central bank digital currency.” Philip Lowe, governor of the RBA, has publicly expressed skepticism about the need to implement a retail CBDC in Australia, but the door is still open to the possibility.

The Bahamas

The Bahamas became the unlikely location of the world’s first nationwide CBDC when they launched the “Sand Dollar” back in October 2020. The island archipelago—with one of the highest per capita incomes in the Americas and a 90% mobile device penetration rate—was viewed as an ideal laboratory for the CBDC experiment by central bankers and hyped as a harbinger of a “new world economy” by the global financial press. . . .

But the banksters have not been thrilled with the results so far. The IMF told the Central Bank of The Bahamas earlier this week that it needs to “accelerate its education campaigns and continue strengthening internal capacity and oversight” of the currency.

Brazil

Roberto Campos Neto, president of the Central Bank of Brazil, confirmed last month that the bank will be running a pilot test of its CBDC, the digital real, before the end of the year. “This is a way to create currency digitization without creating a break in bank balance sheets. This project should have some kind of pilot in the second half of the year,” Neto said at the press conference announcing the pilot’s launch.

Canada

This past March, the Bank of Canada (BoC) announced that it had partnered with the Massachusetts Institute of Technology (MIT) to “collaborate on a twelve-month research project on Central Bank Digital Currency.” The project—which the BoC describes as “part of the Bank’s wider research and development agenda on digital currencies and fintech”—will “explore how advanced technologies could affect the potential design of a CBDC.” This will in turn “help inform the Bank of Canada’s research effort into CBDC.”

Chile

Chile’s central bank issued a report this week on its plans for a future Chilean digital currency. Spouting the usual bankster platitudes about how a CBDC “would contribute to achieving a competitive, innovative and integrated payment system that is inclusive, resilient and protects people’s information,” the review ultimately concludes that “a deeper analysis of the benefits and risks” is in order, and promises (or threatens, depending on your perspective) to issue a new report on the subject toward the end of the year.

In the meantime, the Chilean Central Bank governor, Rosanna Costa, has said that Chile’s CBDC “should operate both online and offline” and that it should “allow the authorities to trace the transaction afterwards” while paradoxically “safeguarding personal data.”

China